Award-winning practice management trusted by more than 10,000 accounting firms

For everything to be on one platform, it’s huge. It costs us less money too. Having everything centralized in TaxDome helps us, and it helps the client.

5 Min

IRS Form 5472 is a US tax form for foreign-owned corporations engaged in US trade or business. You can find out everything you need to know about the form in our straightforward guide on Form 5472.

In short, you will need to file Form 5472 if your business is:

- A US corporation with 25% or more of its stock owned by a non-US person or entity

- A US disregarded entity with 25% or more of its stock owned by a non-US person or entity

- A foreign corporation conducting trade or business in the US

If one of these applies to your business, here’s a simple but complete guide on how to fill out Form 5472 with step-by-step instructions.

Initial steps

If your business needs to file Form 5472, the first step is to prepare the required information. This includes legal information about your corporation, its foreign shareholders and related parties.

The next step is knowing the deadline for filing Form 5472. Form 5472 must be filed as an attachment to your income tax return, so the deadline for filing Form 5472 is the same as the deadline that’s required for your income tax return.

Lastly, decide whether you want to file Form 5472 by mail or electronically:

- To file Form 5472 by mail, file it to the same address that’s required for your income tax return

- To file Form 5472 electronically, file it through an Approved IRS Modernized e-File (MeF) Business Provider

How to file Form 5472: a step-by-step guide

Form 5472 is a three-page form, with nine parts and a total of 52 lines that can be filled in. However, you might not need to fill in all of Form 5472, as some parts and lines will not apply to all businesses.

Here are all nine parts of Form 5472, which we will go over in more detail in the next sections:

- Reporting Corporation

- 25% Foreign Shareholder

- Related Party

- Monetary Transactions Between Reporting Corporations and Foreign Related Party

- Reportable Transactions of a Reporting Corporation That Is a Foreign-Owned U.S. D.E

- Nonmonetary and Less-Than-Full Consideration Transactions Between the Reporting Corporation and the Foreign Related Party

- Additional Information

- Cost Sharing Arrangement (CSA)

- Base Erosion Payments and Base Erosion Tax Benefits Under Section 59A

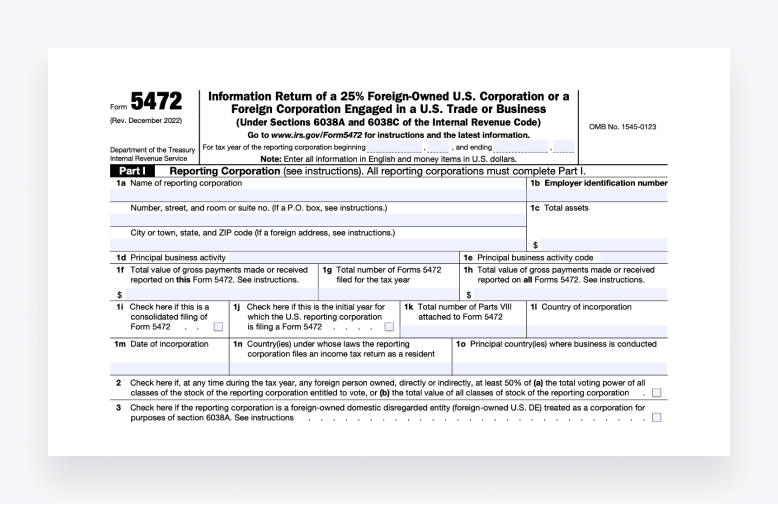

Part 1: Reporting Corporation

Part I of Form 5472 must be completed by all reporting corporations. It covers the essential details about the reporting corporation and its business activity, including the total value of gross payments made or received.

- Lines 1a–1e: Fill in the essential details about the reporting corporation, including the business name, address, Employer Identification Number (EIN), principal business activity and principal business activity code

- Lines 1f–1h: State the total value of gross payments made or received that are reported on this form (line 1f), as well as all forms if you are filing multiple forms (Form 5472) for the tax year (line 1h). State the number of forms that are being filed for the tax year in line 1g

- Lines 1i–1k: Check line 1i if this is a consolidated filing of Form 5472, and check line 1j if this is the first filing of Form 5472 for the reporting corporation. In line 1k, state the total number of cost sharing arrangements (CSA) attached to the form in Part 8 (you can return to this later)

- Lines 1l–1o: For these lines, fill in the country of incorporation for the reporting corporation, the date of incorporation, the country where the reporting corporation files its income tax returns, and the principal country where the reporting corporation conducts business

- Line 2: Check the box if any foreign person in the reporting corporation owned at least 50% (directly or indirectly) of the voting power of all classes of stock, or at least 50% of the total value of all classes of stock

- Line 3: Check the box if the reporting corporation is a foreign-owned US disregarded entity

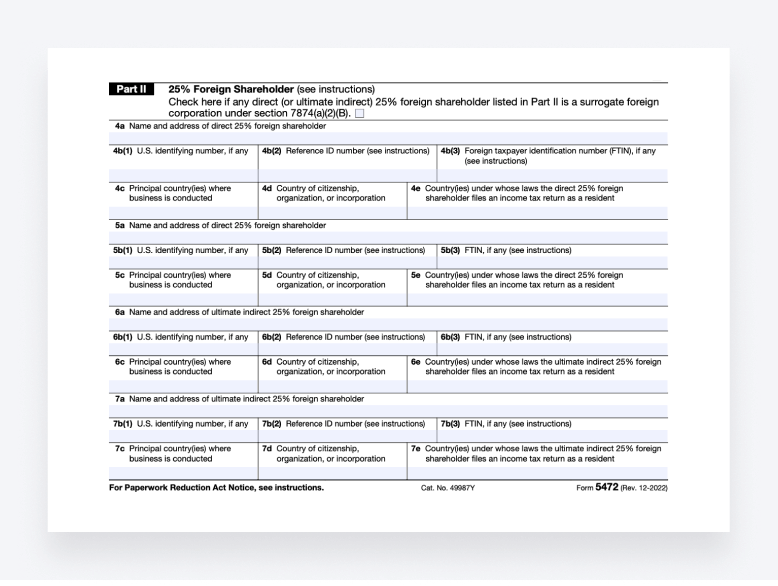

Part II of Form 5472 must be completed by all reporting corporations with 25% foreign shareholders. Depending on the number of 25% foreign shareholders, fill in lines 4–7 with the required information, which includes:

- Name and address

- US identifying number, reference ID number, and foreign taxpayer identification number (FTIN)

- Principal country or countries where business is conducted, country of citizenship, and the country where the 25% foreign shareholder files their income tax returns as a resident

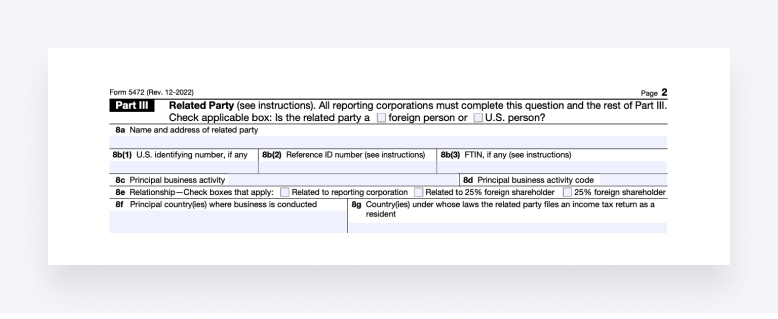

Part III must be completed by all reporting corporations. This is to provide details about related parties, which can include direct or indirect 25% foreign shareholders, relatives of the 25% foreign shareholder, or a person who is related to the reporting corporation.

- First, check the box to state whether the related party is a foreign person or US person

- Line 8a: Fill in the name and address of the related party

- Lines 8b(1–3): Provide the US identifying number, reference ID number, and foreign taxpayer identification number (FTIN)

- Lines 8c and 8d: Fill in the principal business activity and principal business activity code

- Line 8e: Regarding the relationship of the related party, check the boxes that apply

- Lines 8f and 8g: State where the principal country or countries where the related party’s business is conducted, and where the related party files income tax returns as a resident

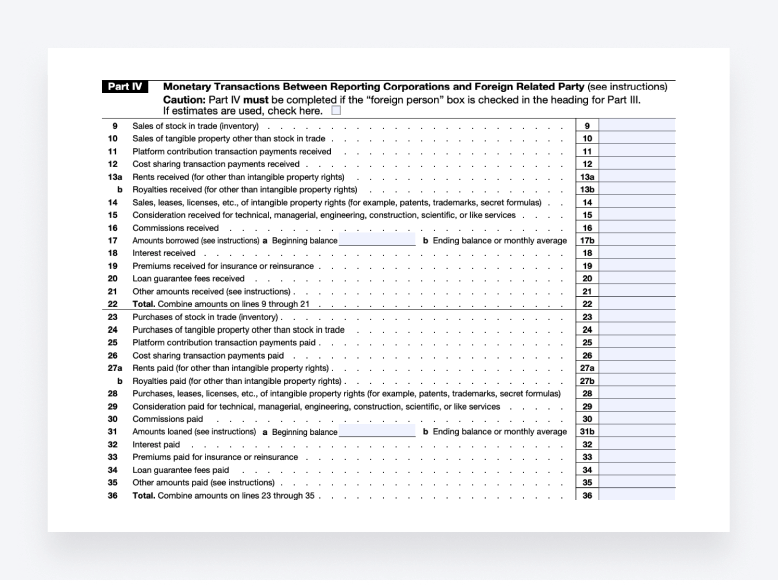

Part IV of Form 5472 is for reporting monetary transactions between the reporting corporation and a foreign related party.

Take note: Part IV must be completed if you checked the “foreign person” box at the top of Part III.

Part IV has a total of 30 lines (lines 9–36). However, the first 15 lines (9–22) are sales-related while the last 15 lines (23–36) are purchase-related.

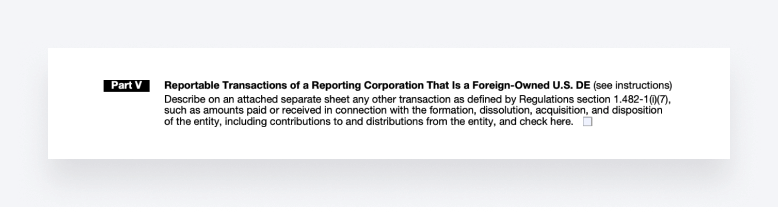

Part 5: Reportable Transactions of a Reporting Corporation That Is a Foreign-Owned U.S. D.E

Part V of Form 5472 only applies to foreign-owned US disregarded entities.

For paid or received transactions (including contributions and distributions) that are not reported in Part IV, this section requires foreign-owned US disregarded entities to check the box and describe these transactions on an attached sheet.

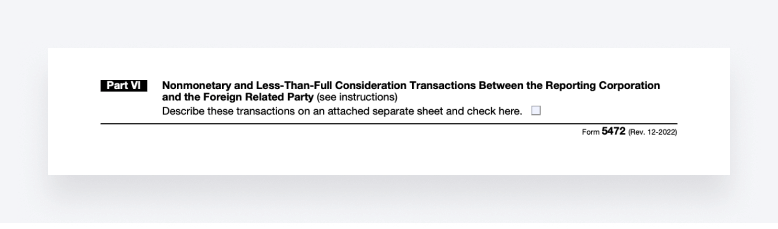

Part VI of Form 5472 applies to reporting corporations that had nonmonetary transactions with foreign related parties.

Like Part V, these must be described on a separate sheet attached to Form 5472. If this applies to the reporting corporation, check the box and make sure to attach the required information.

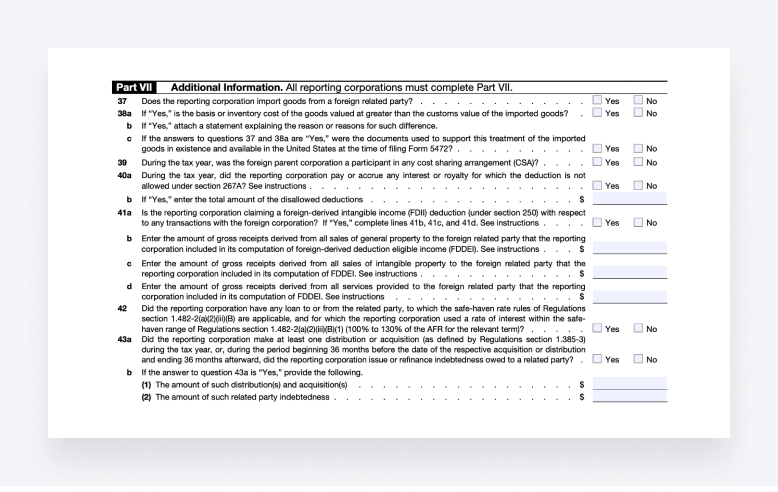

Part 7: Additional Information

Part VII of Form 5472 is for providing additional information about the reporting corporation. These are self-explanatory questions, with “Yes” or “No” checkboxes or blank fields for declaring monetary amounts.

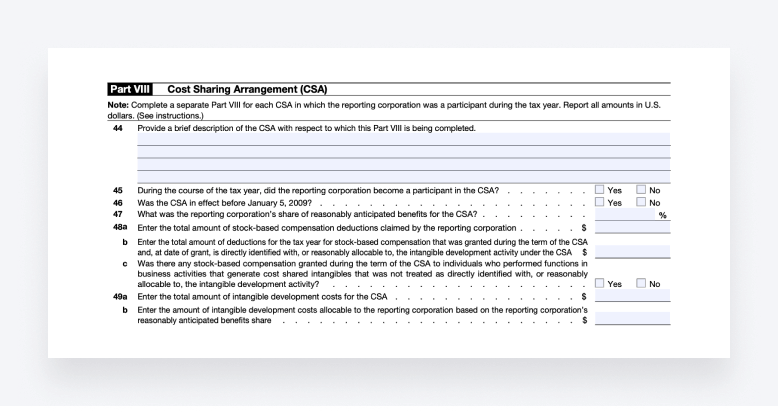

Part 8: Cost Sharing Arrangement (CSA)

Part VIII of Form 5472 is for providing information on all cost sharing arrangements (CSA) that the reporting corporation participated in during the tax year. A separate Part VIII must be completed for each cost sharing arrangement.

- Line 45: Fill in a description of the CSA

- Line 46: Check “Yes” or “No” if the reporting corporation became a participant in the CSA during the tax year

- Line 47: Check “Yes” or “No” if the CSA was in effect before January 5, 2009

- Lines 48a–48c: Report amounts (in US dollars) regarding stock-based compensation deductions claimed by the reporting corporation

- Lines 49a and 49b: Report amounts (in US dollars) for intangible development costs regarding the CSA and reporting corporation

Remember: For all cost sharing arrangements (CSA) that you provide for this section, make sure to state the total number in line 1k of Part I.

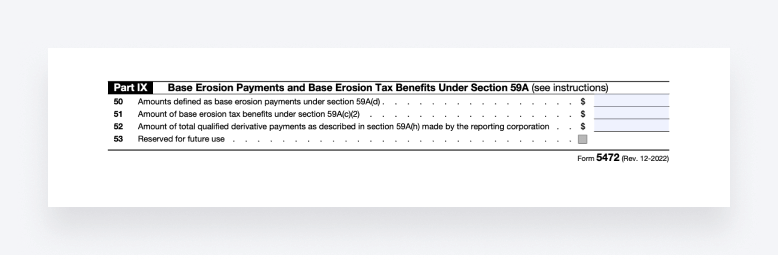

Part 9: Base Erosion Payments and Base Erosion Tax Benefits Under Section 59A

Part IX of Form 5472 is for providing the amounts for:

- Base erosion payments (line 50)

- Base erosion tax benefits (line 51)

- The total qualified derivative payments made by the reporting corporation (line 52)

Lastly, check the final box on line 53 if it applies to the reporting corporation.

And that’s it – you’ve completed the final section of Form 5472.

Reportable transactions

Reporting transactions with foreign related parties is an important component of Form 5472, and you must provide these in Part IV – most importantly if you checked “foreign person” at the top of Part III.

The IRS defines a reportable transaction as:

- Any type of transaction listed in Part IV (for example, sales, rents, etc.) for which monetary consideration (including U.S. and foreign currency) was the sole consideration paid or received during the reporting corporation’s tax year;

- Any transaction listed in Part V; or

- Any transaction or group of transactions listed in Part VI.

Reportable transactions that are inaccurate or missing from Form 5472 can result in receiving a penalty from the IRS. So, it’s important to report all transactions with foreign related parties accurately, including paid and received transactions.

The exception is the payment of dividends, which does not need to be reported to the IRS.

Avoiding common errors on Form 5472

Errors on Form 5472 can result in penalties for failure to file “in the manner described, for failure to maintain records, and for failure to submit information or filing false or fraudulent information.”

This can result in receiving a $25,000 penalty from the IRS (per Form 5472) and an additional $25,000 penalty if failure to fail continues for more than 90 days.

So, it’s well worth double-checking the requirements and the information you have provided on Form 5472 before filing it.

Common errors on Form 5472 include:

- Missing reportable transactions: Make sure to provide all reportable transactions accurately, which includes all monetary considerations paid or received during the tax year

- Missing the deadline: Make sure to file Form 5472 with your income tax return and its associated deadline

- Missing documentation: Make sure to include supporting documentation where required, as well as keep supporting documentation on file in the event it is requested by the IRS

- Missing information: Make sure to fill in all the required information on Form 5472 that that applies to your business

Finalizing and submitting Form 5472

Once you have filled out Form 5472, finalize by double-checking the information you have provided for inaccuracies. For added peace of mind, you can consult a tax professional to review the form for you before filing it.

To submit Form 5472, file it with your income tax return. The address and deadline for filing Form 5472 will therefore be the same as the required address and deadline for filing your income tax return.

What to do if you make a mistake on Form 5472

If you have made a noticeable mistake on Form 5472, which hasn’t been filed, it’s a good idea to obtain a new form and start again. The quickest way to obtain a new Form 5472 is to download it from the IRS website and print it out.

If you think you have made a mistake after filing Form 5472, it’s best to contact the IRS directly to avoid any issues – including penalties. The IRS may ask you to resubmit Form 5472 with the amended information and a written explanation of the mistakes and your corrections.

Conclusion

To wrap up, you’ll need to file IRS Form 5472 if you own a corporation with at least 25% foreign ownership, or a foreign corporation that trades and does business in the US.

It’s important to both fill out and file Form 5472 correctly too, as failing to do these can result in notifications from the IRS and even penalties.

Just as with other IRS forms, if you need assistance with Form 5472, you can always turn to a tax professional or business adviser for personalized advice.

Josef Hynard

Josef is a content writer for TaxDome who enjoys creating clear, actionable content to inspire readers about TaxDome’s features and updates. When he’s not fitting words together, he likes to read books and work out.

Thank you! The eBook has been sent to your email. Enjoy your copy.

There was an error processing your request. Please try again later.

Looking to boost your firm's profitability and efficiency?

Download our eBook to get the answers