Award-winning practice management trusted by more than 10,000 accounting firms

For everything to be on one platform, it’s huge. It costs us less money too. Having everything centralized in TaxDome helps us, and it helps the client.

7 Min

Given the complexity of tax regulations, the potential for tax avoidance or evasion has always been high. To counter this threat, the IRS requires material advisors to disclose any reportable transactions they are involved in using Form 8918.

In this article, we’ll explain everything you need to know about IRS Form 8918, including:

- What it’s for — and when you might need to use it

- How to fill it out

- Common mistakes to avoid

- Legal implications for failing to use it correctly

Understanding IRS Form 8918

The IRS has two forms that are used for disclosing reportable transactions: Form 8886, which is for taxpayers, and Form 8918, which is for material advisors. But what exactly is a material advisor?

The IRS defines a material advisor as any individual or entity that:

- Provides material aid, assistance, or advice with respect to the organizing, managing, promoting, selling, implementing, insuring, or carrying out of any reportable transaction, and

- Directly or indirectly receives or expects to receive gross income in excess of the threshold amount for the material aid, assistance, or advice

Beyond all the industry jargon, the purpose of Form 8918 is quite simple — to enhance compliance and transparency in tax reporting. Its origins can be traced back to legislative measures introduced in the early 2000s in response to growing concerns about tax avoidance schemes, including the Reportable Transactions Penalty Act of 2004 and the Internal Revenue Code (IRC) Section 6111.

By mandating the disclosure of reportable transactions by material advisors, Form 8918 enables the IRS to gather essential information about potentially abusive tax schemes and identify areas of non-compliance more effectively.

Criteria for filing Form 8918

Form 8918 should be completed by any material advisor involved in a reportable transaction that exceeds certain threshold amounts. Where the reportable transaction provides tax benefits to an individual, the threshold is $50,000. For all other transactions, the threshold amount is $250,000, with lower thresholds for listed transactions (more on this below).

A reportable transaction is any transaction that the IRS deems to have a high potential for tax avoidance or evasion. They fall into one of the following five categories:

1. Listed transactions

These are transactions that are the same or substantially similar to one of the items described in the official IRS list of recognized abusive and listed transactions. For listed transactions, the threshold amount is lowered from $50,000 to $10,000 for individuals and from $250,000 to $25,000 for all other transactions.

Example: One of your clients leased a property and then immediately subleased it back to themselves (listed as a lease in/lease out, or LILO, transaction).

2. Confidential transactions

There are transactions where a taxpayer enters a confidentiality agreement with an advisor, and the advisor receives a minimum fee for their services. The minimum fee is $250,000 for a corporation (excluding S corporations) and $50,000 for other entities and individuals.

Example: You entered a confidentiality agreement with a client relating to a certain transaction and earned a fee of $75,000 for your services.

3. Transactions with contractual protection

This refers to a transaction where the taxpayer is entitled to a partial or full refund of any fees if all or part of the intended tax benefits aren’t realized.

Example: A transaction failed to realize the intended tax benefits for one of your clients, and as a result, they were contractually entitled to a refund of the fees paid to you.

4. Loss transactions

Loss transactions refer to transactions that lead to a taxpayer claiming a loss under Section 165 of the IRC. A Section 165 loss allows the taxpayer to deduct losses, sustained during a taxable year, that are not covered by insurance or other means.

For such a loss to be considered a reportable transaction, it must meet one of the following criteria:

- Individuals: at least $2 million in any tax year or $4 million in any combination of tax years

- Corporations (excluding S corps): at least $10 million in any tax year or $20 million in any combination of tax years

- Partnerships with only corporations (excluding s corps) as partners: at least $10 million in any tax year or $20 million in any combination of tax years

- All other partnerships and S corps: at least $2 million in any tax year or $4 million in any combination of tax years

- Trusts: at least $2 million in any tax year or $4 million in any combination of tax years

Example: You acted as an advisor to an individual taxpayer who claimed a Section 165 loss of over $2 million in the last tax year.

5. Transactions of interest

These are transactions that the IRS deems to have the potential for tax avoidance or evasion, but for which there isn’t sufficient evidence to prove that the transaction should be identified as tax avoidance.

Example: You acted as an advisor to a US taxpayer who owns a foreign trust or partnership through another US entity.

Instructions on how to complete Form 8918

In this section, we’ll guide you through the process of filling out Form 8918 step by step. For more detailed guidance, please refer to the official IRS instructions.

First of all, you need to provide details about the materials advisor, including their:

- Name

- Address

- Telephone number

You’ll also be asked to specify whether the material advisor is an individual or an entity by checking the respective box. If you check the entity box, you’ll also need to fill in the name, title, and telephone number of the contact person (item A).

Next, it’s time to disclose all relevant information about the reportable transaction.

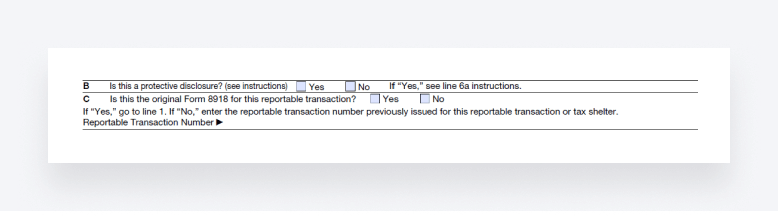

Item B: you’ll need to specify whether this is a protective disclosure or not. If it is, you’ll need to follow the instructions for line 6a.

Item C: you’ll also need to specify whether this is the original form for this reportable transaction. If it’s an amendment to a previously filed Form 8918, select “no” and enter the original reportable transaction number provided by the IRS.

Line 1: Next, enter the name of the reportable transaction — i.e. what type of transaction it is. If no name officially exists, provide a short description instead that distinguishes it from other reportable transactions.

Line 2 and 3: check the relevant box or boxes to determine the category of reportable transaction that applies — and follow the instructions if you checked boxes “a” or “e”.

Line 4: enter the date that you became a material advisor to the reportable transaction. This should be whichever of the following dates came most recently:

- The date you made a tax statement relating to the transaction

- The date you received — or expected to receive — income over the threshold amount

- The date the transaction was entered into by your client

- The date the transaction became a listed transaction or transaction of interest

Line 5: if you entered into a designation agreement with other material advisors for this reportable transaction, you can identify any other parties here, including names, addresses, and contact details. There’s only space for one additional material advisor here, so if you need to add more, you can attach additional sheets.

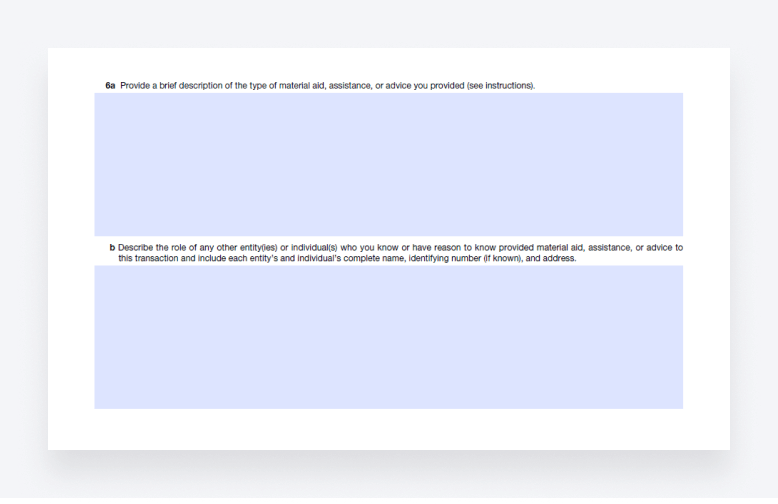

Line 6a: In this section, you’ll need to provide a brief description of the service you provided to become a material advisor for this reportable transaction. For protective disclosures, you’ll have to explain why you believe you are not a material advisor.

Line 6b: If you know about any other individuals or entities that are material advisors to this reportable transaction, you can provide their names, identifying numbers, and addresses here.

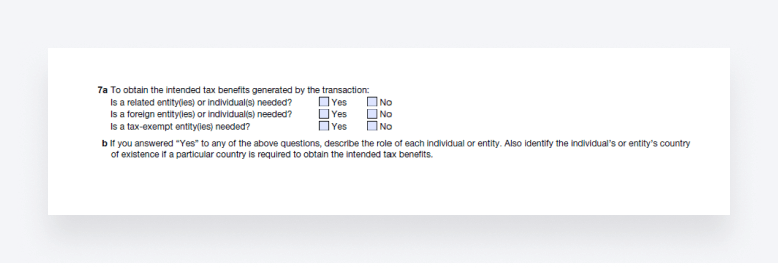

Line 7a: Check “yes” or “no” for each question in this section.

Line 7b: If you checked “yes” for any of the questions above, you’ll need to provide additional information here. For example:

- Who are the related parties, and how are they related?

- How and why is a foreign entity or individual needed, and which country are they based in?

- What is the role of any tax-exempt entities or individuals in the reporting transaction?

Line 8a and 8b: Like line 7, check “yes” or “no” for this question. If you checked “yes”, you’ll need to provide additional information about the roles of entities or individuals in the reporting transaction.

Line 9: In this section, you’ll list the types of financial instruments used in the transaction. This could include a loan, stocks, bonds, notes, currency agreements, swaps, futures, or any other kind of instrument.

Line 10: Here, simply check all the relevant tax benefit boxes that apply to this reportable transaction.

Line 11: If you checked a box in line 10, you’ll need to select one of the options relating to the period in which the tax benefits are to be claimed.

Line 12: Enter the relevant sections of the IRC under which your client claimed any tax benefits relating to this transaction.

Line 13: Lastly, write down all the relevant facts about the reportable transaction, including the following information:

- The tax benefits that caused the transaction to be reportable

- The years that relate to the transaction

- Key steps of the transaction — e.g. agreements, transfers, acquisitions, sales

- How each step helped achieve the tax benefits

- The nature of the transaction — e.g. cash, loan, service

- How each party to the transaction was involved, and what their roles were

- The business or financial reasons for the transaction

- How the financial instruments were used in the transaction

- How the IRC sections enabled the tax treatment to be achieved

This is a critical part of the form, and we recommend reading the relevant section of the official IRS instructions to ensure that you have everything covered.

Finally, it’s time to sign and date the form.

Common mistakes to avoid during completion

Completing Form 8918 accurately is crucial for material advisors to comply with reporting requirements and avoid potential penalties (more on those later!). To help you along the way, here are some common errors to avoid.

Failure to disclose all reportable transactions

As a material advisor, you must accurately identify and report each reportable transaction you are involved in, including those that may seem insignificant or routine.

Incorrectly classifying transactions

Misclassifying transactions can lead to inaccuracies in reporting. It’s important to understand the criteria for different types of reportable transactions (e.g. listed transactions, confidential transactions) and ensure that they are correctly classified on Form 8918.

Incomplete or inaccurate information

Providing incomplete or inaccurate information on Form 8918 can result in delays or errors in processing. Remember to carefully review the form and provide all required information accurately. If in doubt, refer to the official IRS instructions.

Missing deadlines

Failing to file Form 8918 by the deadline can lead to penalties and enforcement actions by the IRS. Familiarize yourself with the filing deadlines for Form 8918 and make sure you submit your form on time.

Ignoring updates or changes to reporting requirements

The IRS may update reporting requirements or guidelines for Form 8918 periodically. Be sure to stay informed about any changes or updates to ensure compliance with current reporting requirements. Also, make you use the most up-to-date version of the form, or your filing will be rejected.

Filing requirements and deadlines

In this section, we’ll look at the requirements around when, where, and how to file Form 8918.

Deadlines

You should file Form 8918 with the Office of Tax Shelter Analysis (OTSA) by the last day of the month following the end of the quarter in which you became a material advisor. So, if you became a material advisor on February 1, 2024, the deadline would be April 30, 2024.

Submission methods

There are two methods for filing Form 8918: electronic fax and mail. For electronic fax, you should fax to 1-844-253-5607. Your fax cover sheet should also include the following key information:

- Subject: Form 8918

- Information about the sender (you): name, title, phone number, and address

- The name of the material advisor (again, you)

- The date you are sending it

- The number of pages included, including the cover sheet

Note: don’t include any sensitive information on the cover sheet, such as an EIN or social security number.

For regular mail, you can use the OTSA address found on page 4 of the IRS instructions under the “Where to file” section.

Legal implications and penalties

If you fail to file Form 8918 before the deadline, or if your form includes inaccurate or incomplete information, you could pay a hefty fine.

For reportable transactions other than listen transactions, the penalty is currently $50,000. For listed transactions, it’s whatever is the larger amount between $200,000 or 50% of the gross income you received as a material advisor to the listed transaction, or 75% if the failure is deemed intentional.

If you are required to maintain a list by the IRS and fail to make it available within 20 business days, there’s a $10,000 fine for every day after the 20th business day, until the obligation is fulfilled. There are also additional penalties imposed by various sections of the IRC — we recommend looking at the official IRS instructions for more information here.

FAQs about Form 8918

We’ve covered a lot of ground in this article, but in case you still have some questions that need answering, let’s wrap this up with some FAQs.

What is IRS Form 8918?

IRS Form 8918 is a disclosure form used by material advisors to report certain reportable transactions. It helps the IRS monitor and regulate potentially abusive tax schemes and ensure compliance with tax laws.

Who qualifies as a “material advisor”?

A material advisor is an individual or entity that provides advice, assistance, or services in connection with any reportable transaction.

What types of transactions need to be reported on Form 8918?

You can use Form 8918 to report various types of reportable transactions that the IRS has identified as having potential for tax avoidance or evasion. These include listed transactions, confidential transactions, transactions with contractual protection, and transactions resulting in significant tax losses.

When is the deadline to file Form 8918?

Generally, the form must be filed by the last day of the calendar month following the end of the quarter in which you became a material advisor to the reportable transaction.

Can Form 8918 be filed electronically?

Yes, you can file Form 8918 using electronic fax.

What are the penalties for failing to file Form 8918 or filing it late?

Penalties for non-filing, late filing, or incomplete filings of Form 8918 are $50,000 for non-listed transactions and at least $200,000 for listed transactions — and can go much higher depending on the amount of income you received as a material advisor. There are additional penalties set out by the IRC as well.

What amount of fees obligates me to file Form 8918?

Material advisors are required to file Form 8918 if they receive fees exceeding certain thresholds for providing advice, assistance, or services related to reportable transactions. See the “Criteria for filing Form 8918 ” section of this article for more information.

What information do I need to include about the reportable transaction on Form 8918?

Material advisors must provide detailed information about the reportable transaction on Form 8918, including its nature, participants, tax benefits sought, and other relevant details. See the “Instructions on how to complete Form 8918” section of this article for more information.

Can I amend a previously filed Form 8918?

Yes, material advisors can amend a previously filed Form 8918 to correct errors or provide additional information. The amended form should indicate that it is an amendment to a previously filed form and include the corrected or supplemental information.

As a material advisor, you are required to maintain a list identifying each individual or entity that you assisted in relation to a reportable transaction. This list must be maintained for seven years from the date on which you made a tax statement relating to the transaction, or the date on which the transaction was last entered into — whichever occurred first.

Conclusion

IRS Form 8918 plays a key role in ensuring tax compliance and transparency for material advisors. It’s not the simplest form to complete, but it’s one of the most important. Failure to do so could result in severe fines or worse.

We hope this guide has provided you with all the information you need to make disclosures to the IRS accurately and effectively.

Nicholas Edwards

As a content writer for TaxDome, Nicholas helps communicate how technology can transform and enhance everyday accounting processes. He enjoys simplifying complex ideas and writing content that’s accessible and useful.

Thank you! The eBook has been sent to your email. Enjoy your copy.

There was an error processing your request. Please try again later.

Looking to boost your firm's profitability and efficiency?

Download our eBook to get the answers