Award-winning practice management trusted by more than 10,000 accounting firms

For everything to be on one platform, it’s huge. It costs us less money too. Having everything centralized in TaxDome helps us, and it helps the client.

8 Min

Accounting technology has replaced manual paperwork with software platforms that allow accountants and firms to do more for their clients in less time.

This increased efficiency has led 90% of accountants to believe that technology will drive their firm’s future growth. Additionally, accountants at firms that offer integrated accounting technology are 80% more likely to stay with their current firm.

Knowing this, it becomes clear why staying up to date on new technology trends in accounting is essential. In this article, that’s just what we’re going to explore: the accounting technology trends you need to know more about in 2024.

What is accounting technology?

Accounting technologies are the systems, software and tools designed to manage and process financial information. They include any digital solutions used in preparing, reviewing, and reporting financial data, such as:

- Bookkeeping

- Payroll processing

- Tax preparation

- Budgeting

- Financial reporting

- E-filing taxes

Depending on the scope of a specific accounting tool, it can also encompass communication with clients, including securely sharing financial documents, collecting e-signatures and receiving payment for services.

Accounting technology has a long history. However, you’re likely more familiar with the digital transformation, in which solutions have emerged that automate manual data entry and curb the necessity of physically storing vast amounts of paper documents.

Now, with the emergence of AI (artificial intelligence), blockchain technology and the continued adoption of mobile apps, accounting technology is entering a whole new era.

Top accounting technologies

The 2020s are set to reach new heights in technological advancements that impact the workplace. Accounting technologies that enable further automation will free up time for financial professionals to work on higher-level tasks.

So, with that in mind, here are the accounting technology trends that are worth watching in 2024:

- Artificial intelligence (AI) in accounting

- Cryptocurrency and blockchain technology

- Data security in accounting

- Workflow automation

- Mobile accounting apps

1. Artificial intelligence (AI) in accounting

AI is rapidly changing operations in a slew of industries, and current studies show that 2024 is likely to be a defining year for generative AI. Within accounting, artificial intelligence has already significantly impacted process automation, data accuracy, client experience and data-driven insights.

Examples

QuickBooks has embraced AI and already offers several AI-powered features, including:

- An AI receipt scanner that links pertinent information to existing expenses or accounts

- Cash-flow predictions

- Algorithms that help calculate small business funding options

This is just one company in the accounting and finance world that’s leveraging the power of AI. Industry powerhouses, such as KPMG, Deloitte and PwC, are also using AI to automate document reviews, improve audit accuracy and help brainstorm for the future.

Challenges

As with any great stride forward, there are always bumps in the road to be mindful of. AI systems require large volumes of high-quality data for effective learning and accurate outcomes. This takes time.

Additionally, AI isn’t updated in real-time, so the information it operates on is limited to its last update. Because of this, it’s not a perfect source for information on current tax laws and regulations.

Future trends

Though many feared AI would render their job obsolete, attitudes are changing. More than 60% of business and technology leaders report excitement about the prospect of generative AI, and 56% are using it to improve efficiency and productivity.

With fear subsiding and its benefits becoming clearer, accounting and AI are due for a strengthened partnership in 2024 with firms and individuals continuing to experience how they can help improve their processes.

If you want to learn more about using AI in accounting, read “AI in accounting: exploring opportunities and real-life examples.”

2. Cryptocurrency and blockchain technology

Blockchain technology refers to a decentralized ledger system that records transactions across multiple computers, securing the ownership transfer of assets. Cryptocurrency is, as the name suggests, a digital currency that operates on a blockchain to ensure transparency, security and the integrity of transaction data.

With more clients using or investing in cryptocurrency, it’s valuable for accountants to have some knowledge about the digital currency to better understand its tax implications. Additionally, by enhancing security through its transparent ledger system, blockchain technology can impact the landscape of finance and accounting by changing how assets are transferred between institutions and individuals.

Examples

Sites like Coinbase, Binance and even Fidelity enable clients to buy and sell cryptocurrency. Going forward, accounting professionals will need to learn more about how to help clients involved in the crypto space. Cryptocurrency accounting firms are already popping up to meet the needs of these clients.

Blockchain technology has accounting implications beyond cryptocurrency. Thanks to its secure and transparent ledgers, blockchain technology could significantly reduce the risks of data manipulation and theft without accounting firms.

Blockchain technology can also help automate bookkeeping and reconciliation work, reducing the costs to reconcile and maintain ledgers. This will affect individuals primarily involved in these tasks as firms opt to utilize blockchains to free up accountants’ time and have them focus on higher-level tasks.

Challenges

The regulatory environment for cryptocurrencies is still evolving, with different countries having varied stances and rules. Also, the high volatility of cryptocurrencies can complicate accounting practices, especially in areas like valuation, profit and loss reporting, and tax calculations.

Blockchain technology can face scalability and transaction speed issues, which are critical for large-scale accounting applications. It also takes a considerable amount of energy to power blockchains, creating an energy efficiency issue in a world increasingly concerned about sustainability. So, while these accounting technologies prove exciting and promising, there’s still work to be done before the worldwide public will be ready to embrace them.

Future trends

Cryptocurrency and blockchain technology are a vital part of accounting technology in 2024 because they’re in their infancy and will continue to grow in capability. As the technology matures and the conversation continues around regulations, these technologies will gain further legitimacy and more widespread adoption. The likely question regarding cryptocurrency and blockchain technology is not “if” but “when”.

Blockchain technology will likely continue to improve its functionality, working to increase its efficiency and use cases while making progress in solving its sustainability challenges. As it makes strides, it’s possible that blockchain-based accounting will emerge in the future to tighten security around financial transactions. Take a look at the video below to learn more about blockchain’s future implications on security and the exchange of money around the world.

Bitcoin’s spot ETF, potential institutional investors and central bank digital currencies (CBDCs) are also worthwhile topics to look into for the future of cryptocurrency and blockchain technology in the financial world.

3. Data security in accounting

With accountants handling sensitive financial and personal data, security is always a concern. To address data security issues in accounting, firms use encryption, two-factor authentication and regular security audits to keep their clients’ valuable data safe.

With the average data breach cost approaching $9.5 million dollars in the US, accounting firms must stay diligent when it comes to providing clients with adequate data security.

Examples

So, what can accounting firms do in 2024 to enhance data security?

- Cloud accounting platforms utilize advanced encryption methods both in transit and at rest

- Many accounting software options offer two-factor authentication that verifies client identity through a second factor like a text message, email, or notification through an app

- Accounting firms are offering regular cybersecurity training and awareness programs to their employees

- Many accounting firms have also adopted client portals that use encryption and secure login protocols to exchange sensitive financial documents

Challenges

Despite regular advancements in security, cybercriminals will always be proactive in pursuing valuable accounting and financial data. Spoofing attempts, leaks from third-party vendors and new malware designed to hold your accounting firm’s data hostage are all constant concerns for those who manage others’ financial information.

Additionally, increased demand for remote working accountants further exacerbates the security concerns surrounding remote work, such as lack of security awareness, unsecured connections and using unmanaged personal devices to access client or firm data.

Future trends

Looking forward, accounting firms should look into security systems that offer zero trust architecture (ZTA), an approach to cybersecurity that eliminates implicit trust. This can be especially helpful as more accountants work from home, helping to mitigate the added security risks that come with remote work.

Additionally, as cybercriminals use AI to assist in password cracking, software disruption and creating deepfakes, looking into defensive AI can help accounting firms stay ahead of hackers looking to access their clients’ financial information.

4. Workflow automation

Workflow automation software streamlines and automates various tax preparation and filing aspects. Depending on the specific software, it can simplify data input, form completion and electronic filing.

As accounting firms look to grow by taking on more clients, workflow automation software will become increasingly necessary in 2024 to efficiently manage increased workloads while maintaining accuracy.

Examples

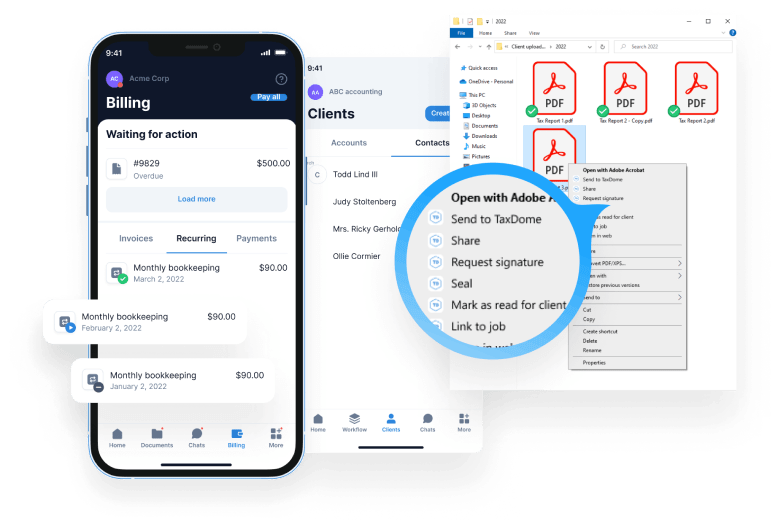

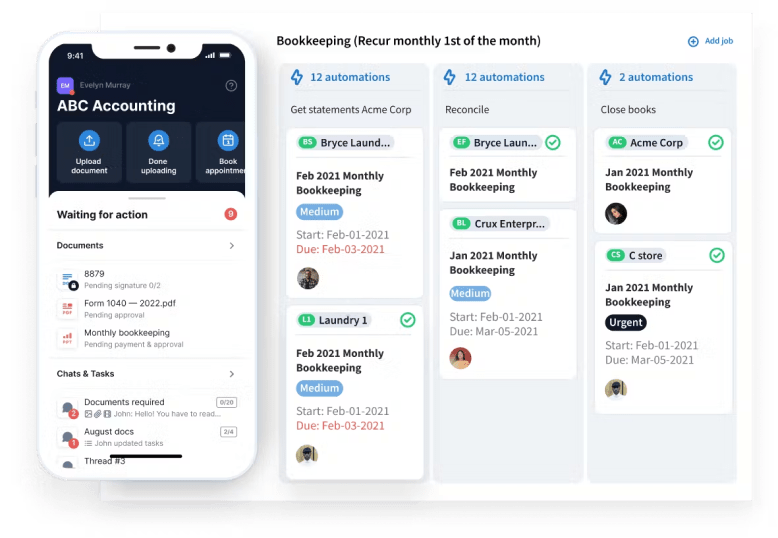

Professional accountants already know about programs like QuickBooks, but to help with scaling, growing firms need practice management software that offers a single source for secure document upload and organization, assigning and tracking tasks, client communication, job audit trails, e-signatures, and invoicing.

Having all of this in one place streamlines firm operations while also conglomerating several accounting tools into one. This makes it easier for accountants to gain an organized overview of their tasks, customize their automation to meet each client’s unique needs, and keep everything in a secure location.

As workflow automation software for the accounting industry continues to advance, it will help accountants manage an ever-increasing workload and grow their practices.

Challenges

Tax laws and regulations are always in flux, so tax software is constantly working to keep up. That’s why using technology that’s known for staying current and evolving to meet changing needs is vital.

Integration also presents challenges. While the most advanced tax and practice management software out there can integrate with one another, as software functions change, so must its integrations. The best solution for this is finding software offering a range of capabilities to minimize the number of integrations needed for a fully operational accounting workflow.

Future trends

Expect more advanced AI capabilities for accounting workflow, personalized tax planning and predictive analysis. Machine learning algorithms can analyze past data to offer tailored tax-saving strategies and forecast future tax implications based on trends, enabling accountants to offer this information to clients.

The shift towards cloud-based platforms in accounting is set to grow as well, which will continue to improve collaboration between tax professionals and clients. If you haven’t already shifted toward a cloud-based solution for your firm, there’s still time in 2024 to embrace what will become the norm for accounting firms throughout this decade and beyond.

5. Mobile accounting apps

As mobile usage continues to rise, clients will gravitate more toward firms that offer convenient mobile accounting apps that simplify their part in the tax preparation process. Mobile accounting apps allow clients to upload vital tax documents, communicate with their accountants and even sign their tax returns from their smartphones or tablets.

This is convenient for accountants as well since clients will be readily available for communication and document uploading from anywhere at any time and accountants won’t need to wait until they have time to sit down at their computer to complete needed tasks.

Examples

Major tax brands like H&R Block, TurboTax and even the IRS offer self-filers options to do their taxes independently from convenient mobile apps. Companies like Xero allow users to run their small business bookkeeping from anywhere by being able to reconcile bank transactions and view cash flow from their app.

Sensing the increased need for mobile solutions, many other accounting and practice management software companies are also continuing to develop apps that help professionals connect with their clients in a more user-friendly way, whether it’s communicating with chat features that deliver messages right to clients’ mobile devices or even allowing them to scan essential tax documents with their phone or tablet’s camera.

Challenges

Designing an intuitive user interface that caters to both professionals and individuals with limited accounting knowledge is crucial for the success of accounting apps. Clients want something straightforward and navigable, while accounting professionals need something that gets them the information they need and helps them organize everything into an easy-to-manage workflow while also providing robust security.

Also, as with software, apps must continually update to address any changes to tax laws or other regulations regarding the secure transmission of private data.

Future trends

The focus will be on creating mobile-friendly interfaces that provide a similar level of functionality for both accountants and clients as desktop software while also offering more advanced features, such as voice user interfaces for communication, that make it easier for clients to communicate with their accountants while they’re on the go.

Mobile accounting apps will also look to increase their ease of use for accountants as it becomes an increasingly remote job. Cutting-edge mobile apps will make it possible for accountants to securely manage documents, request signatures and track job progress while they’re away from their computers.

Benefits of accounting technology

The benefits of using accounting technology can be felt in the time saved executing tasks, streamlined communication and the increased cash flow from serving more clients than in the past without increasing workload. Embracing accounting technology:

- Improves accuracy and reduces errors through automation

- Enhances data security through encryption, two-factor authentication and other emerging security features

- Saves money on increased personnel costs and costs associated with human errors

- Offers opportunities to make data-driven decisions

- Helps accounting firms scale their business by being able to take on more clients

- Enhances collaboration between team members by increasing access to firm data through a centralized repository

- Enables global accessibility and eliminates the constraints caused by team members and clients living in different places

Training and education in accounting technology

With the industry changing as new tools continue to become an increasingly important part of practices, accounting professionals need to upskill and learn about the accounting technologies they’ll work with in the future. The best way to do this is by seeking out learning opportunities.

The American Institute of Certified Public Accountants (AICPA) offers a two-part webcast on AI for accounting and finance professionals that covers the ins and outs of AI, its applications and advantages, and creating data-driven AI strategies. It also offers a certificate program that covers the fundamentals of cybersecurity for accounting and finance professionals.

For workflow software and mobile apps, most services offer comprehensive educational programs on how to customize their platforms for your accounting firm’s specific needs and how to use them to their fullest potential. Many universities with accounting programs also offer classes tailored explicitly toward accounting technology and helping individuals learn how to use these tools.

If you’re interested in learning more about blockchain technology and its implications in accounting, UC Berkeley’s ExecEd program offers a six-week online course that covers current trends and emerging developments in blockchain, cryptocurrency and decentralized finance that will help you learn how to leverage this advanced and emerging technology to your advantage.

Conclusion

The impact of technology on accounting is indisputable. It has streamlined traditional practices and opened new avenues for analysis, strategy, security and business growth. As we look toward the future, the trajectory of accounting technologies promises even more significant transformations, making it an exciting time for professionals in this field.

If you’re ready to learn more about accounting practice management software that can streamline your firm’s operations, join a live demo of TaxDome.

Jeff Nichols

Jeff is a content writer who works in the SaaS and B2B space, particularly in invoicing and accounting. He enjoys helping businesses make informed decisions that will assist them in growing and reaching their goals. As a writer at TaxDome, Jeff creates content that helps customers better understand the platform and stay informed about developments in the accounting industry.

Thank you! The eBook has been sent to your email. Enjoy your copy.

There was an error processing your request. Please try again later.

Looking to boost your firm's profitability and efficiency?

Download our eBook to get the answers