Share this post

Award-winning practice management trusted by more than 10,000 accounting firms

For everything to be on one platform, it’s huge. It costs us less money too. Having everything centralized in TaxDome helps us, and it helps the client.

Ensuring accurate and reliable financial reporting is achieved by diligently following a set of accounting principles. In this guide, we’ll explore the most widely-recognized ones, looking not only at what they entail but also the role they play in enabling stakeholders to effectively assess an entity’s performance and prospects.

What are accounting principles?

Accounting principles are the fundamental concepts that dictate how financial information gets recorded, calculated, and communicated within a company. Their key purpose is to standardize the process so that the resulting financial statements are consistent and transparent.

In the accounting world, there are two main sets of principles that act as guiding lights:

- Generally Accepted Accounting Principles (GAAP), developed and regulated by the Financial Accounting Standards Board (FASB) for companies based in the United States

- International Financial Reporting Standards (IFRS), a globally-recognized set of standards overseen by the IFRS Foundation and the International Accounting Standards Board (IASB)

While GAAP and IFRS have some differences, they share the common goal of promoting uniformity, comparability, and reliability. By following these principles, organizations can provide investors, creditors, and regulators with accurate and useful financial information.

A complete overview of basic accounting principles

Now let’s dive deeper into some of the core accounting principles that underpin financial statements:

1. Historical cost principle

The historical cost principle states that assets and liabilities must be recorded at their original purchase cost or acquisition value in the financial statements.

For example, if a company buys equipment for $50,000, that amount becomes the asset’s recorded cost, regardless of whether the market value fluctuates over time due to inflation, technology changes, etc.

Following this concept promotes objectivity and enables year-over-year comparisons of how resources are utilized. It allows stakeholders to analyze performance trends rather than dealing with constantly shifting valuations.

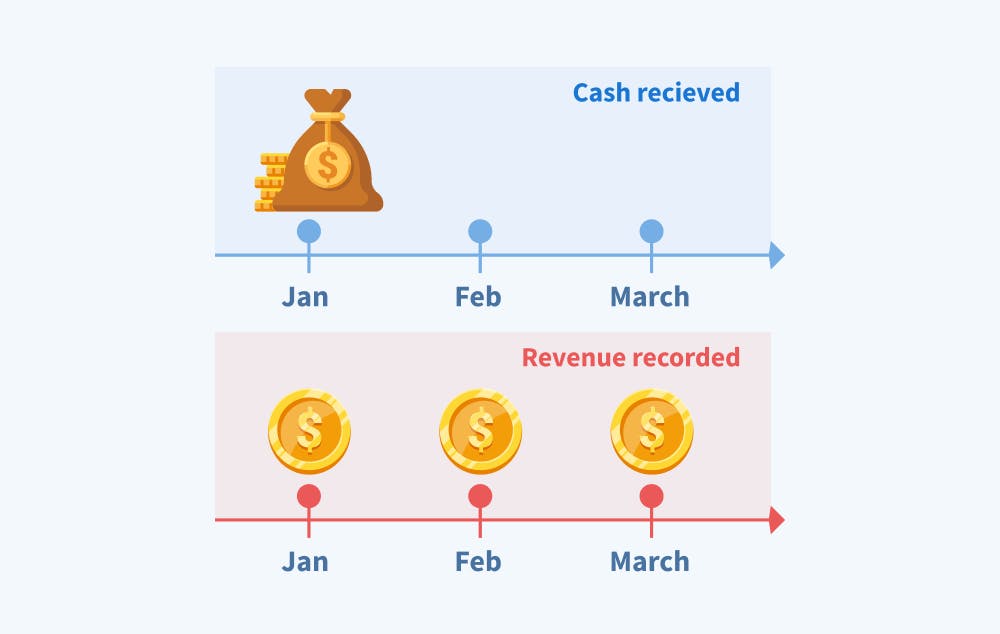

2. Revenue recognition principle

This principle says it should only be recognized when it is realized, realizable, and earned — not just when cash is received.

For example, a software company selling a $1,200 annual subscription would record $100 in monthly revenue as the services are delivered each month, not the full $1,200 upfront.

Properly applying revenue recognition prevents the inflation of profits. It gives stakeholders a realistic measure of a company’s earning power and reduces the risk of revenues being artificially over- or under-stated.

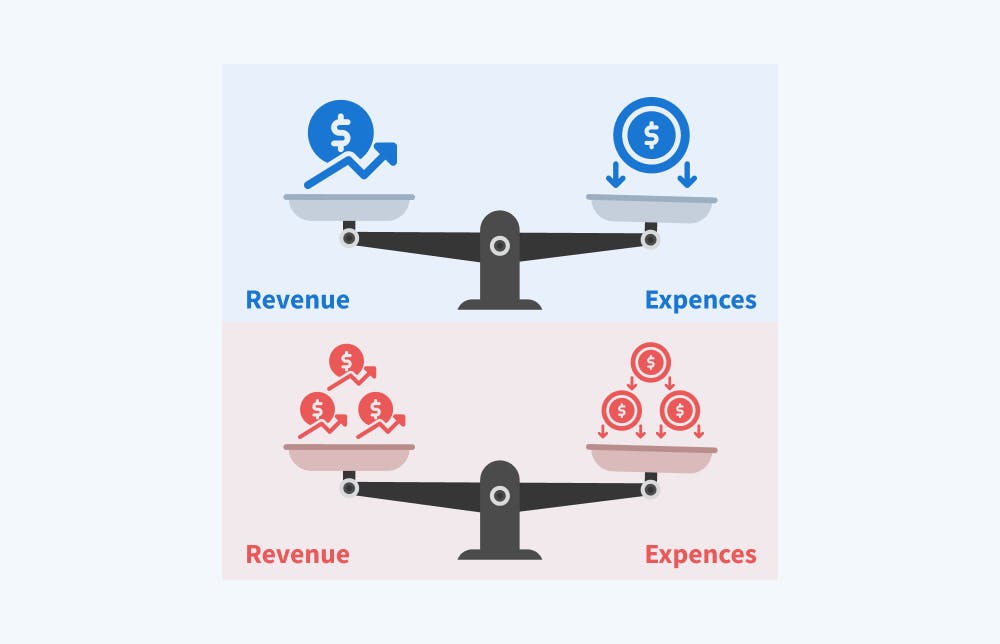

3. Matching principle

Also called the expense recognition principle, the matching concept requires that expenses be recorded and matched with the specific revenues they helped generate in the same reporting period.

For example, if a retailer spends $5,000 on a 6-month advertising campaign that generates $50,000 in sales, the $5,000 expense would be recorded as $833 each month, matched to the incoming revenue.

Following this principle allows stakeholders to evaluate factors such as operational efficiency, pricing strategies, and overall periodic profitability. It promotes alignment between how money is spent and how it gets earned.

4. Full disclosure principle

The full disclosure principle states that all relevant financial details must be disclosed, either directly on the formal statements or in accompanying notes. This could include accounting policies, asset valuation methods, debt obligations, contingencies, and anything else that provides important context.

For example, a pharmaceutical company launched a promising new medication. To fully disclose, they’d detail projected revenue, marketing costs, expected market share, and any other information that gives insight into this opportunity’s potential financial impact.

This transparency provides stakeholders with insights into a significant growth opportunity and how it may positively impact the company’s future financial position.

5. Objectivity principle

Objectivity is the name of the game when it comes to financial reporting. This principle requires that financial information be accounted for and reported in an unbiased, impartial manner — completely free from any influences of personal opinions, preconceived notions, or subjective biases.

For example, if a company invests heavily in developing cutting-edge new products and services, they need to objectively report the substantial increase in research and development costs.

Following this principle ensures stakeholders get a clear view of the organization’s real financial standing and operational activities during that period.

6. Materiality principle

While thoroughness is appreciated, cluttering up financial statements with immaterial details benefits no one. The materiality principle states that information should only be disclosed if it’s significant enough that its omission could influence the decisions and assessments of stakeholders.

For example, a large manufacturing company replaces just a few minor pieces of equipment at one factory location. While part of their day-to-day operations, the relatively small investment would be immaterial compared to their overall massive asset base.

By following this rule, stakeholders can avoid getting caught up in small details when assessing the overall financial situation.

7. Consistency principle

Consistency, consistency, consistency — that’s the core of this principle. Once an organization opts for a particular accounting method or policy, it must be consistently applied across all reporting periods. No switching things up from year to year or quarter to quarter.

For example, a company chooses to depreciate its machinery using the straight-line method, with $10,000 in annual depreciation expense for each $100,000 asset. They must stick to that same depreciation method and schedule year after year until the assets are fully depreciated.

Applying accounting methods uniformly from period to period is what enables meaningful tracking and trend analysis. Consistency promotes reliable benchmarking.

8. Conservatism principle

The conservatism principle instructs organizations to avoid excessive optimism when dealing with uncertainty. Potential losses or liabilities should be recorded as soon as they are reasonably foreseen. However, contingent gains or revenues cannot be booked until they are virtually assured.

For example, if a company has $100,000 in outstanding receivable but doubts about its collectibility, the conservative stance would be to recognize an allowance for doubtful accounts or write off a portion of the receivable.

By adhering to this principle, financial statements are more likely to reflect a cautious and reasonable estimate of a company’s financial position, safeguarding against potential overstatement of assets or understatement of liabilities.

9. Accrual principle

With the accrual principle, revenue and expense recognition are not connected to the actual exchange of cash. Instead, they get recorded in the specific period when the revenue was truly earned or the expense was actually incurred, regardless of the timing of the cash flows themselves.

While the revenue recognition principle focuses just on the criteria for recording revenue, the accrual principle applies to the timing of recording both revenues and expenses.

For example, if a law firm provides legal services to a client in December but does not receive payment until January of the following year, it should record the revenue in December when the services were rendered, not when the cash was received.

This principle, when followed, allows for profitability evaluations to be based on real economic events rather than merely cash flows, and it paints a realistic picture of a company’s periodic performance.

10. Going concern principle

This principle assumes that an entity will continue operating indefinitely into the foreseeable future, carrying on as a “going concern” unless evidence indicates otherwise.

For example, when preparing financial statements, a software company with a steady stream of recurring revenue and no signs of financial distress would apply accounting methods based on the assumption of an indefinite lifespan.

Only organizations facing a crisis such as bankruptcy or a planned termination of operations would depart from the going concern assumption. Otherwise, financial statements presume the entity will keep operating long-term, allowing stakeholders to properly assess the value of its assets, liabilities, and overall positioning from that perspective.

Conclusion

At their core, accounting principles exist to instill transparency, consistency, and ultimately confidence in an organization’s financial reporting. By following guidelines, including the historical cost principle for asset valuation or the revenue recognition rules that align profits with actual performance, stakeholders gain access to accurate and useful financial data.

Adhering to these long-standing accounting fundamentals ensures the numbers don’t mislead but instead provide a faithful representation of the underlying finances. It’s what allows financial statements to be meaningfully analyzed, compared, and acted upon with confidence.

Mari Sam

Mari Sam is a content writer at TaxDome who is passionate about crafting compelling copy. Her job is to ensure that TaxDome clients fully utilize the platform's latest features and enhancements. Through clear communication of updates, changes, and new capabilities, Mari produces engaging content that enables clients to make the most out of the platform.

Thank you! The eBook has been sent to your email. Enjoy your copy.

There was an error processing your request. Please try again later.

Looking to boost your firm's profitability and efficiency?

Download our eBook to get the answers